📊 𝗣𝗿𝗶𝘃𝗮𝘁𝗲 𝗺𝗮𝗿𝗸𝗲𝘁𝘀 𝗳𝘂𝗻𝗱𝗿𝗮𝗶𝘀𝗶𝗻𝗴 𝗿𝗲𝗯𝗼𝘂𝗻𝗱𝗲𝗱 𝗶𝗻 𝟮𝟬𝟮𝟱 — 𝗯𝘂𝘁 𝘁𝗵𝗲 𝗿𝗲𝗮𝗹 𝘀𝘁𝗼𝗿𝘆 𝗶𝘀 𝘀𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗮𝗹.

Our latest whitepaper, “𝘛𝘩𝘦 𝘙𝘪𝘴𝘦 𝘰𝘧 𝘗𝘦𝘳𝘱𝘦𝘵𝘶𝘢𝘭 𝘊𝘢𝘱𝘪𝘵𝘢𝘭: 𝘙𝘦𝘴𝘩𝘢𝘱𝘪𝘯𝘨 𝘗𝘳𝘪𝘷𝘢𝘵𝘦 𝘔𝘢𝘳𝘬𝘦𝘵𝘴 𝘍𝘶𝘯𝘥𝘳𝘢𝘪𝘴𝘪𝘯𝘨,” examines what’s driving divergence across asset classes and why semi-liquid evergreen structures are becoming the new normal.

𝗞𝗲𝘆 𝗶𝗻𝘀𝗶𝗴𝗵𝘁𝘀:

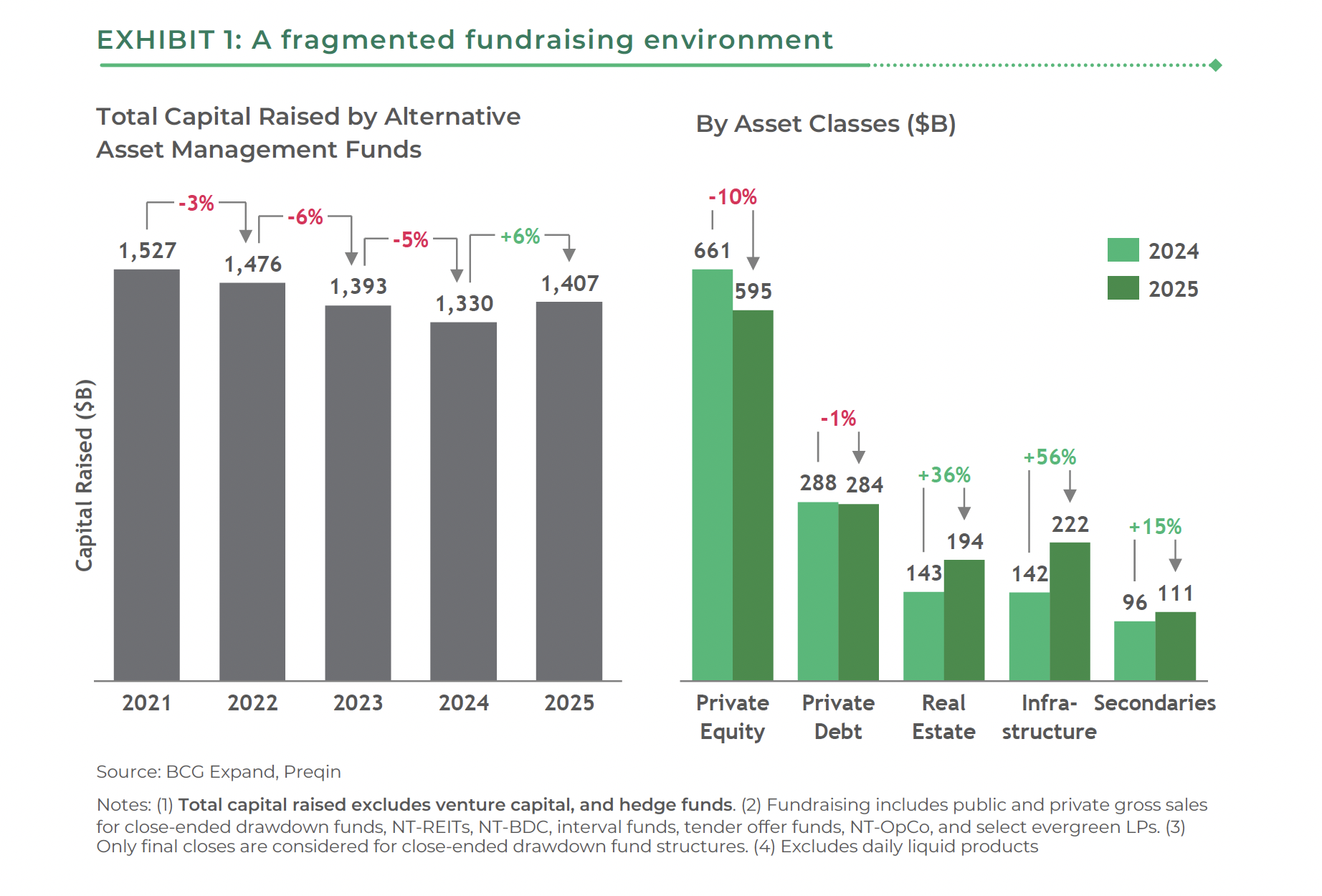

🌍 Private capital fundraising hit $1.4T in 2025 — the first rebound after three consecutive years of decline, though recovery remains uneven across asset classes.

🔄 Semi-liquid evergreen structures are reshaping how private markets capital is raised, with broad-based growth spanning private credit, real estate, infrastructure, and private equity.

🌐 Outside the U.S., regulatory frameworks including ELTIF 2.0 and LTAF are unlocking retail and wealth capital, accelerating product innovation across Europe and the UK.

👉 Read the full whitepaper here

Introduction: A Deeper Look at Private Capital Fundraising

The alternative asset management industry is entering a new phase of structural change. Despite steady AUM growth—expanding at roughly a 6% CAGR since 2021—the fundraising landscape has become increasingly fragmented. In 2025, private capital fundraising rose to $1.4 trillion, marking the first annual increase since the 2021 peak.

Yet the rebound was uneven: private equity and private debt remained subdued, while infrastructure emerged as a standout performer, buoyed by inflation linked demand and energy transition themes.

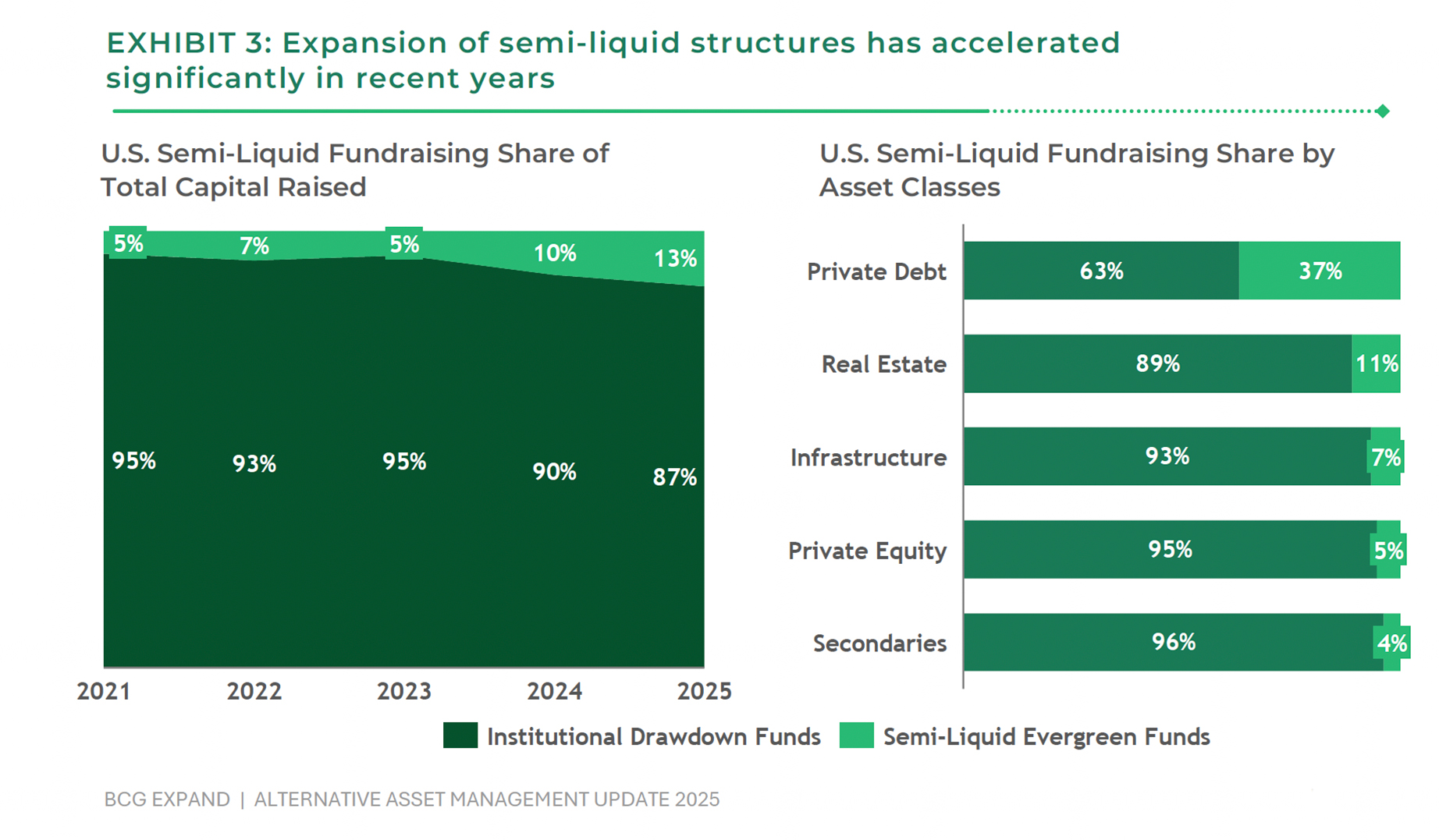

At the same time, the industry is undergoing a fundamental shift in how capital is raised. Semi liquid evergreen vehicles have moved from niche to mainstream, offering General Partners (GPs) a more stable and recurring capital base while providing investors limited periodic liquidity subject to redemption caps. Their adoption has accelerated rapidly—rising from 5% to 13% of U.S. fundraising since 2021—with similar momentum building across Europe and the UK through ELTIF and LTAF regimes. As liquidity constraints persist and wealth channels expand, perpetual capital is increasingly influencing the future of private markets fundraising.

CAPITAL RAISING ACROSS ALTERNATIVE ASSET CLASSES

Divergence, Consolidation, and the Redefinition of Fundraising Channels

Fundraising across private markets in 2025 reflects a highly fragmented landscape, where aggregate stability masks meaningful divergence across asset classes, investor channels, and product structures. While headline capital raised remains resilient, underlying dynamics point to slower deployment cycles, increased concentration of capital towards large GPs, and a structural shift toward semi-liquid evergreen vehicles.

For GPs, the environment is increasingly defined by scale advantages and access to diversified distribution. For limited partners (LPs), selectivity remains high amid macro uncertainty and liquidity concerns.

PRIVATE EQUITY: CONSOLIDATION AND SCALE DOMINATE

PRIVATE EQUITY: CONSOLIDATION AND SCALE DOMINATE

- Private equity fundraising continued to soften in 2025, with total capital raised declining to $595 billion, a 10% YoY decrease. While capital raised declined modestly, number of funds closed was lowest in several years, indicating industry consolidation with fewer but larger funds.

- Capital is increasingly concentrated in larger vehicles. Funds targeting $1 billion or more represent only a small fraction of the overall fund universe (10%), yet they account for a disproportionate share of total capital sought (62%). This reflects LP preference for established managers with proven track records, particularly in an environment where liquidity remains constrained.

PRIVATE DEBT: SEMI -LIQUID STRUCTURES GAIN GROUND AS TRADITIONAL DRAWDOWN FUNDS SLOW

- Private debt fundraising remained broadly flat at $284 billion in 2025, but this stability masks a shift in underlying capital sources. Institutional drawdown fundraising declined, while semi-liquid structures – particularly those targeting wealth channels experienced strong growth.

- Semi-liquid funds accounted for 37% of the total private debt capital raised, with nontraded BDCs continuing to dominate as the preferred access vehicle. At the same time, the rise in interval fund structures signals ongoing product innovation aimed at broadening investor access.

- Investor sentiment has become more cautious. A tighter credit environment, coupled with rising default rates and valuation pressures in certain sectors, has led to increased scrutiny of underwriting standards and manager capability.

REAL ESTATE: RECOVERY AMID STRUCTURAL HEADWINDS

- Real estate fundraising rebounded in 2025, reaching $194 billion and marking a strong 36% YoY increase. The recovery was primarily driven by the successful closing of several mega-funds, alongside stronger capital flows into non-traded REITs

- Despite this uptick, structural challenges persist. Fundraising timelines have lengthened considerably, while expectations of “higher-for-longer” interest rates continue to weigh on investor sentiment and decision-making. Notably, no new nontraded REITs were registered in 2025. Instead, sponsors have concentrated on existing vehicles – optimizing portfolios and exploring alternative capital raising channels, including private offerings and DST programs.

INFRASTRUCTURE: A STANDOUT PERFORMER

- Infrastructure emerged as one of the strongest-performing asset classes in 2025, raising a record $222 billion. Growth was broad-based, spanning both institutional and wealth channels, and supported by macroeconomic tailwinds such as inflation protection and energy transition themes.

- The asset class continues to benefit from increasing fund sizes, with capital increasingly concentrated among large, established managers with proven track records. Megafund closings have played a significant role in driving overall fundraising volumes.

- At the same time, infrastructure is increasingly being packaged into semi-liquid formats, expanding access to a wider investor base.

SECONDARIES: SUSTAINED MOMENTUM IN A LIQUIDITYCONSTRAINED MARKET

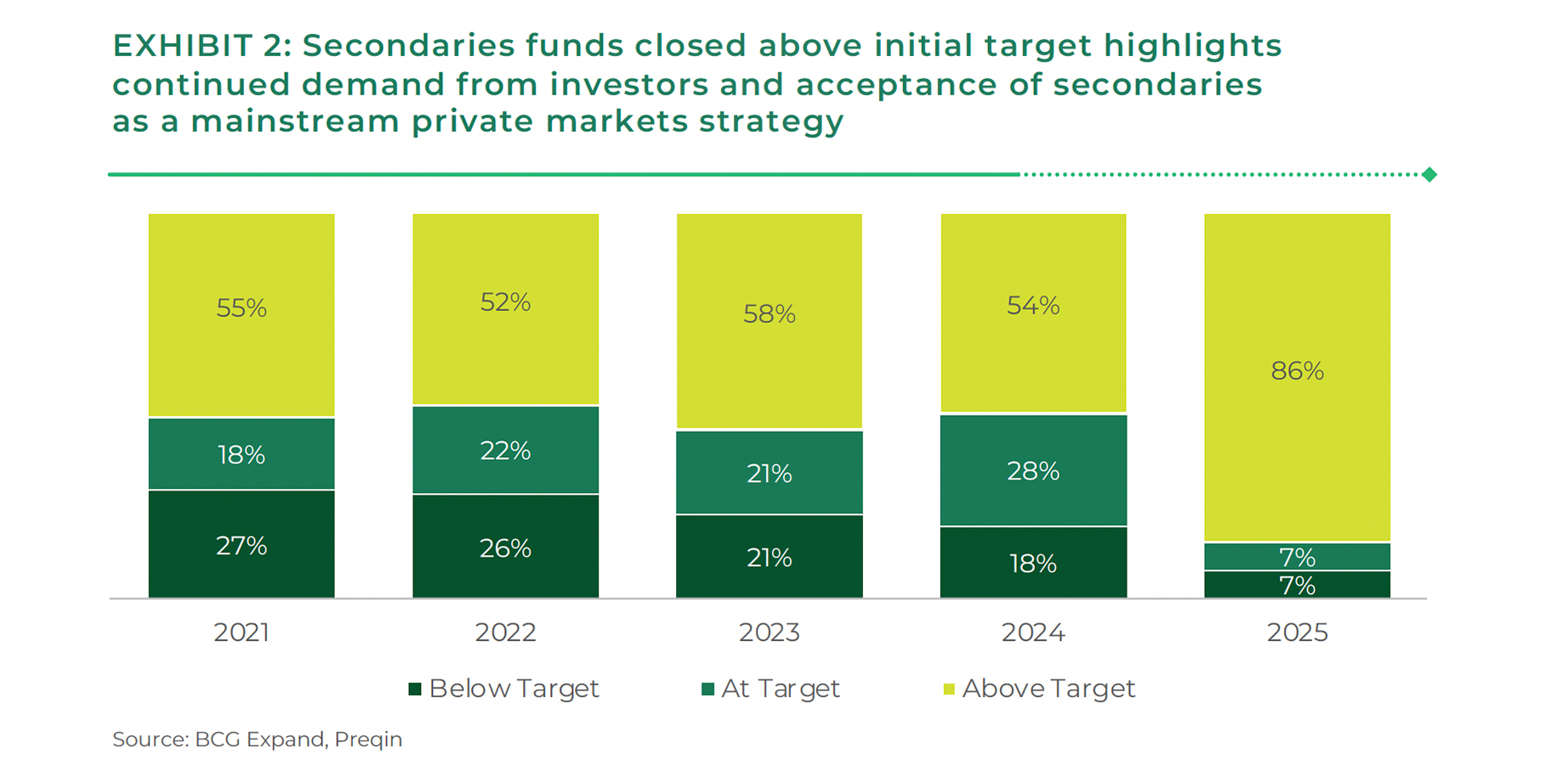

- Secondaries fundraising continued its upward trajectory, increasing 15% YoY. The asset class is benefiting from persistent demand for liquidity solutions, as slower exit activity in primary markets drives increased transaction volume.

- Notably, a growing proportion of secondaries funds are exceeding their fundraising targets – an indication of strong LP demand and confidence in the strategy (see Exhibit 2). Diversified vintage portfolio and reduced J-curve remained key factors for growing demand.

THE RISE OF SEMI-LIQUID FUND STRUCTURES

THE RISE OF SEMI-LIQUID FUND STRUCTURES

A STRUCTURAL SHIFT IN FUND DESIGN

- Semi-liquid fund structures have moved from niche offerings to a central pillar of alternative asset fundraising. Designed to balance periodic liquidity with long-term investment horizons, these vehicles are increasingly being used by GPs to access a broader investor base, particularly within the wealth management channel.

- Unlike traditional closed-end drawdown funds, semi-liquid vehicles (including evergreen funds, interval funds, tender offer funds, and non-traded BDCs/REITs) provide continuous fundraising and deployment capabilities. This enables GPs to build more stable, scalable, and recurring capital bases.

- What was once viewed as product innovation is now becoming a structural evolution in how private markets capital is raised. In the U.S., semi-liquid vehicles have seen substantial growth, with capital raised increasing sharply YoY and now representing a 13% share of total fundraising, up from just 5% in 2021.

- This growth is not confined to a single asset class but is instead broad-based, spanning private credit, real estate, infrastructure, and nascent but increasingly private equity.

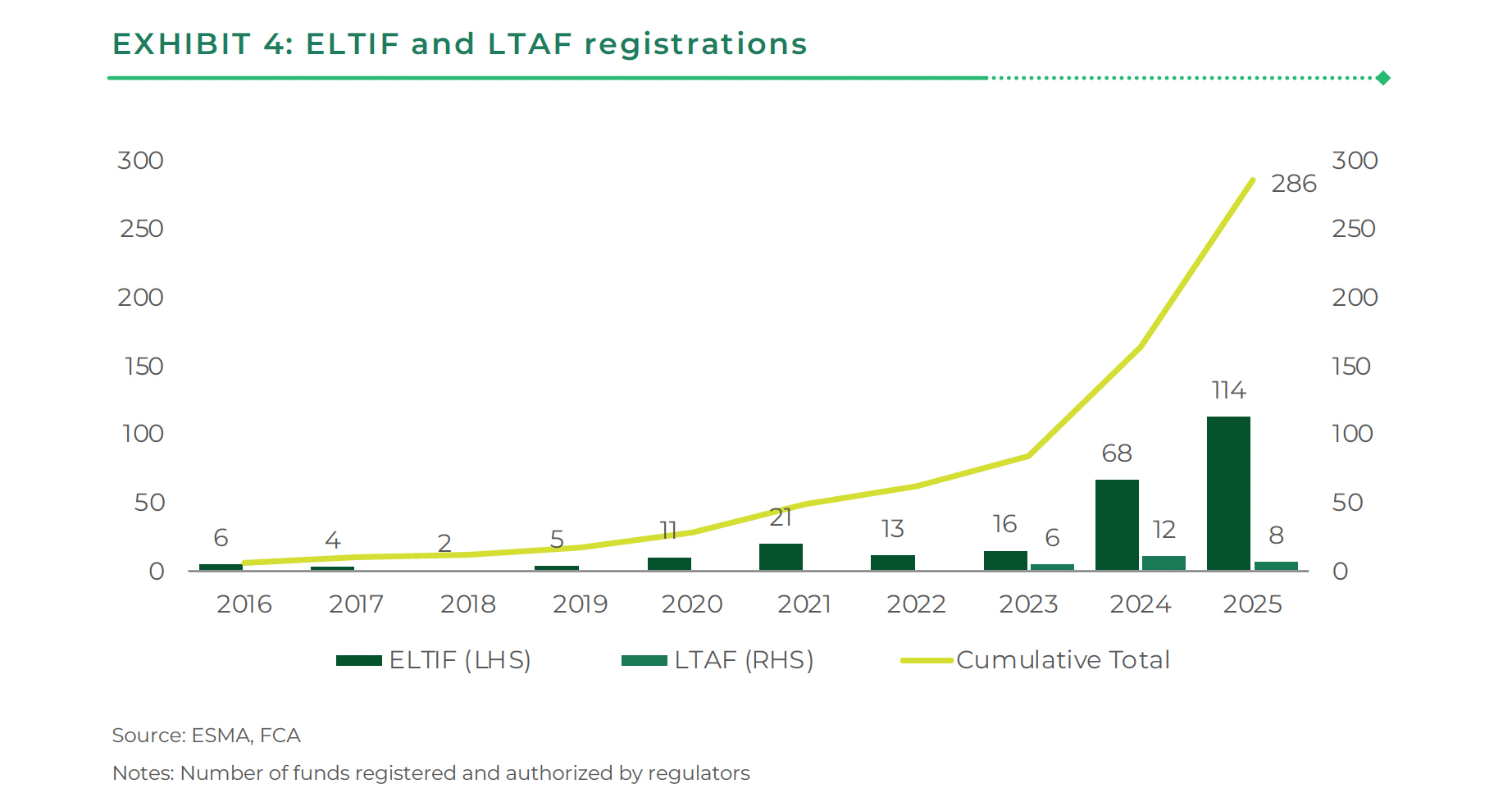

- Outside the U.S., regulatory developments, particularly in Europe and the UK have catalysed adoption through structures such as ELTIFs and LTAFs

NON-U.S. REGISTERED FUNDS: REGULATION AS A GROWTH CATALYST

NON-U.S. REGISTERED FUNDS: REGULATION AS A GROWTH CATALYST

A RAPIDLY EVOLVING PRODUCT LANDSCAPE

Outside the United States, regulatory-driven innovation continues to play a central role in shaping fundraising dynamics. Frameworks such as Part II UCIs, ELTIFs, and LTAFs are enabling broader access to private markets, particularly among retail and wealth investors.

This has led to a surge in product development and cross-border expansion by global asset managers.

PART I I UCI : STRONG GROWTH ACROSS STRATEGIES

The Part II UCI universe expanded rapidly in 2025, with assets and fund counts increasing significantly across private equity, real estate, and fund-of-funds strategies. Large global managers have been early adopters, leveraging the structure to access European investors more efficiently.

ELTIF 2.0: UNLOCKING RETAIL CAPITAL

The revised ELTIF framework has materially improved the attractiveness of the structure, offering greater flexibility and fewer constraints on portfolio construction. As a result, new fund launches have accelerated sharply (Exhibit 4).

Private debt strategies dominate the landscape, reflecting investor demand for yield, followed by private equity and infrastructure offerings.

LTAF: BUILDING MOMENTUM WITH POLICY SUPPORT

The UK’s LTAF regime continues to gain traction, with steady growth in assets and fund launches since inception. While momentum slowed toward the end of 2025, the structure remains a key pillar of the UK’s long-term strategy to democratize private market access. Potential inclusion in tax-advantaged investment accounts could act as a meaningful catalyst for future growth.

CLOSING INSIGHT: A STRUCTURAL SHIFT, NOT A CYCLICAL BLIP

CLOSING INSIGHT: A STRUCTURAL SHIFT, NOT A CYCLICAL BLIP

The evolution of fundraising in alternative assets is no longer cyclical – it is structural. The convergence of longer exit timelines, increased demand for liquidity, and the rise of wealth distribution is reshaping how capital is raised.

Firms that adapt to this new reality by embracing semi-liquid structures, expanding distribution capabilities, and differentiating their value proposition – will be best positioned to succeed in the next phase of private markets.

_____

To explore how BCG Expand supports alternative asset managers with data, benchmarking, and strategic insights, connect with:

Amrit Shahani is a Managing Director in BCG Expand’s London office.

Chirag Shah is a Principal in BCG Expand’s London office.

© BCG Expand 2026. All Rights Reserved.